How Much Do Japanese People Typically Earn, Save, and Borrow?

How Much Do Japanese People Typically Earn, Save, and Borrow?

The Japanese are renown for being frugal savers, but will their nest eggs be enough for the "golden years" of retirement?

Japanese people are renown for being frugal savers, but they also have a healthy habit of taking on a fair degree of household debt relative to financial assets.

People in their 40s have a comparatively large debt burden relative to income and financial assets. During this decade of life many must also cover the cost of secondary and college education for their children and continue to pay-off their homeowner’s loan.

By the time they retire most Japanese have not saved up enough to supplement their national pension, and 1 in 7 are likely to end up with only barely enough to survive.

Although most employers strongly discourage their employees from sharing details about personal compensation, it is routine for fellow associates to compare such data. These discussions often lead to envy and cause one side to think that the old saying “the grass is always greener on the other side” may, in fact, be true.

While 1-to-1 comparisons are ripe for misunderstanding, knowing how you are doing relative to national benchmarks can provide positive motivation. Recently some interesting data were published in Japan by the Central Council for Financial Services Public Relations (金融広報中央委員会) which provide an accurate gauge for judging the financial well-being-or not-of Japanese households.

Are Japanese Savers?

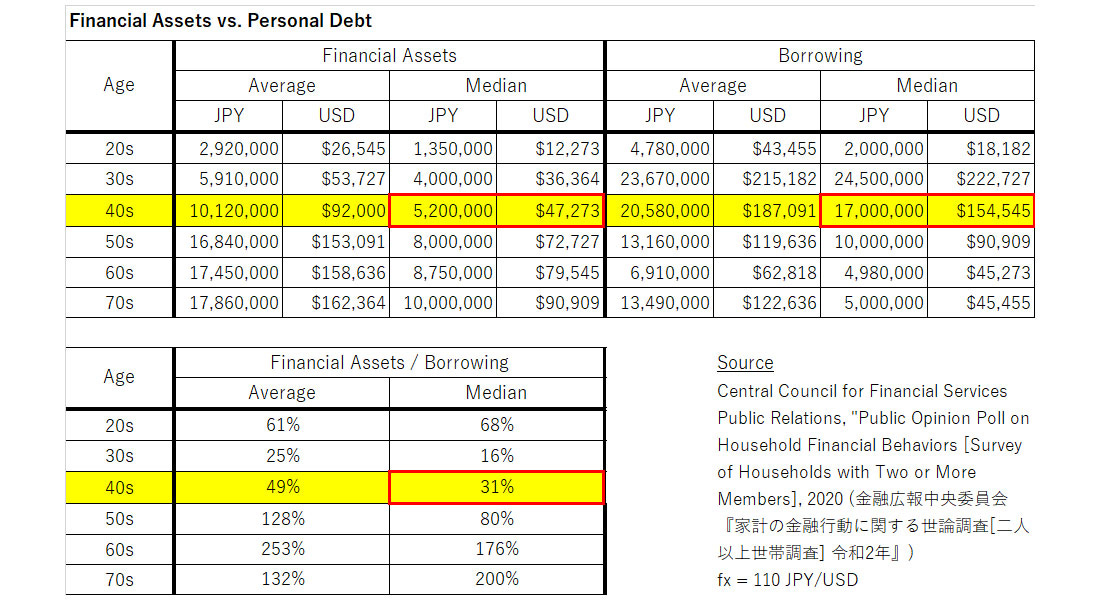

The short answer is, “yes,” especially compared to the citizens of other highly developed industrialized nations. Japanese people are renown for being frugal savers, but they also have a healthy habit of taking on a fair degree of household debt relative to financial assets.

As can be expected, most of this debt is assumed by those in their 30s in the form of a homeowner’s loan. The debt is repaid periodically over the next 20 to 30 years. Savings also grow gradually over time from this point.

Let’s take a closer look at the numbers.

It is, by the way, most telling to focus on median data to avoid the outsized impact on the averages that outliers can cause and to get a true picture of what is the typical experience in Japan.

The variance between financial assets and borrowing is greatest for people in their 30s, which can be expected. It is when many families commit to purchasing their own home and, as a result, obtain a homeowner’s loan. For most this burden extends into their 40s.

With 17 million yen (approximately US $150K) of personal debt and only 5.2 million yen of financial assets ($50K), the ratio of financial assets vs. debt of 31% is significant for those in their 40s. It is at this stage in life when many confront high expenses related to the cost of their children's education, while simultaneously continuing to make loan repayments.

Relatively High Expenses for Those in Their 40s

According to the Ministry of Education, Culture, Sports, Science and Technology's "Survey of Children's Education Costs in Fiscal Year 2008," if a child were to attend a public school from kindergarten to university, the cost would be about 8 million yen ($73K) per child; if the child were to attend a private university, the cost would be about 9 to 10 million yen ($82K to $91K); and if the child were to attend a private school from junior high school on, the cost would be about 14 to 15 million yen ($128K to $137K).

Keep in mind that compulsory education still only goes through middle school for a total of 9 years in Japan. Thus, sending one’s children to private school when they reach high school age is common. There are, moreover, plenty of other expenses such as private tutoring to ensure good test scores. The adage “You get what you pay for” often holds true, and the cost of these supplemental services does not come cheap.

Whether you rent or own your house, the monthly cost of housing also tends to be a heavy burden. Given all of the other expenses for those in their 40s, it is not difficult to imagine that the monthly repayments are not easy.

Given such expenses, take-home pay is critical.

How Much Do 40-Somethings Earn?

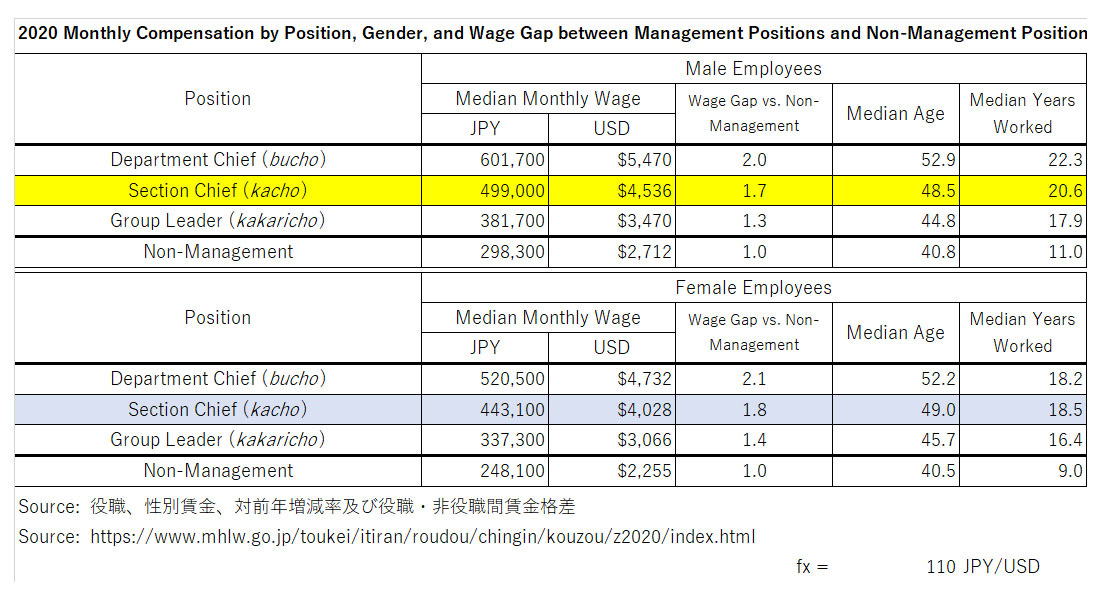

First, like elsewhere, there tends to be a significant gap between the wages of those in management and non-management employees. In Japan there is, moreover, a noteworthy wage difference between men and women.

These differences stand out when comparing median monthly wages.

Taking non-management employees as the baseline, in 2020 median monthly compensation for men was just shy of 300,000 yen ($2,700) among respondents with a median age of 40.8. For women it was just less than 250,000 yen ($2,250) among respondents with a median age of 40.5.

Those in management tend to earn significantly more. Group leaders (kakaricho) tend to make 1.3 ~ 1.4x the salary of non-management employees by the time they reach their mid-40s. Section chiefs (kacho) earn 1.7 ~ 1.8x the salary of non-management associates, although it typically takes until one’s late 40s to reach this level of management. By that point median monthly wages are almost 500,000 yen ($4,500) for men (row highlighted in yellow) and 443,000 yen ($4,000) for women (row highlighted in blue).

Thus, at least for those who have been able to earn promotions and/or job hop their way up the ladder, by about half-way through their career, compensation seems adequate for covering the mounting educational expenses and repaying a homeowner’s loan.

Although single-wage earner families are still common in Japan, especially when augmented by the income of one’s spouse—even if it is only part-time—the primary bread-winner’s salary of a group leader or section chief should be enough to cover both their immediate needs and supplement their national pension after retirement.

Earnings of non-management employees are, however, so low that private school and home ownership are, for the most part, unattainable. For this group the key question is whether they will have enough savings for their “golden years” after retiring.

Prepared for Old Age?

Keeping in mind that the median amount of financial assets among people in their 70s is 10 million yen ($90K), it appears as though most people will have barely enough savings to supplement their national pension and enjoy a comfortable retirement.

Everything is, however, not likely to work out well for the lowest tier earners. They are destined to live at or near the poverty level when elderly. 1 in 7 people in their 40s has take-home pay of only about 160,000 yen (US $1,460) per month and will, therefore, only be eligible for a national pension pay-out of only 100,000 yen ($900) per month from age 65. Especially considering that this group is unlikely to have any savings, trying to make due by living on social security payments alone will be very difficult.

While people with relatively low earnings are, most likely, going to be in trouble, what about the average couple?

If a husband and wife continue to work as full-time employees until they reach retirement age, they would receive a combined monthly pension of 280,000 yen ($2,500). Although dual income households are now common in Japan, it is often difficult for both breadwinners to maintain full employment throughout their earning years. One may change their work style to part-time, or there may be a gap in one of their careers. If this happens, the amount of pension the couple can receive will decrease. In 2020 the average monthly public pension received by an unemployed couple over 65 years old was 218,980 yen ($2,000).

The national pension scheme cannot be expected to cover everything. While expenditures late in life are likely to vary significantly depending upon individual spending habits, private savings will be necessary to make up any shortfall throughout the remainder of each person’s life after retiring.

The So-Called “20 Million Yen Rule”

Although it is not clear whether this figure is pertinent for most, during the past few years numerous media in Japan have reported that a typical worker should have at least 20 million yen ($180K) saved for retirement.

Where did this number come from?

Is such an amount really enough?

Especially considering that the median amount of personal savings per household is only half that amount by around age 70, many couples are anxious about how best to prepare for retirement.

To assess whether the “20 Million Yen Rule” is, in fact, appropriate, expenses must be anticipated.

Expenses Can Add up

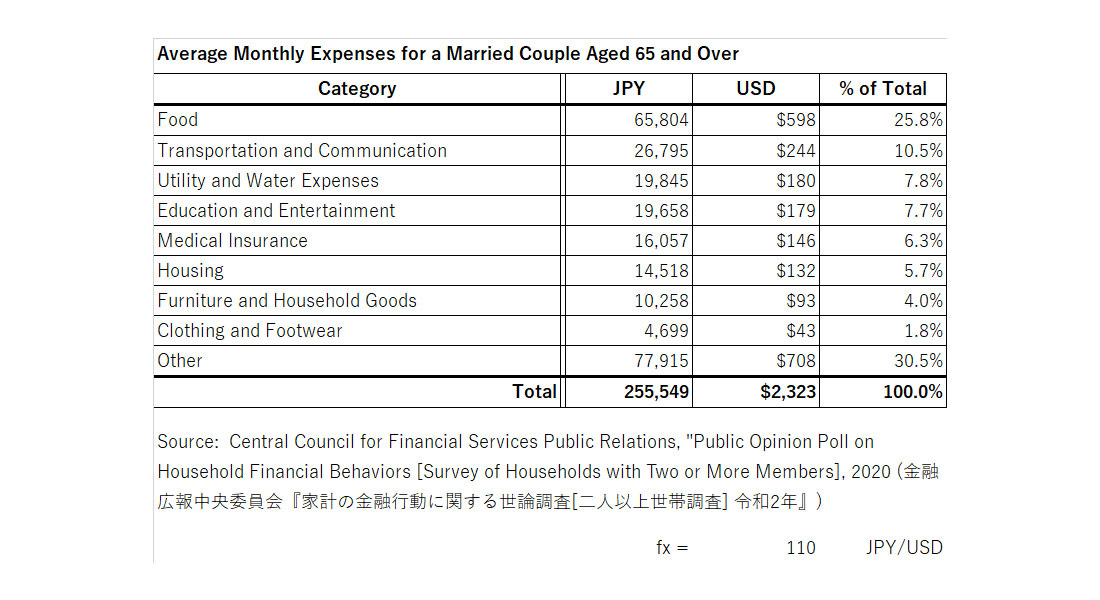

Survey results indicate that the average monthly expenses for a married couple aged 65 and over total approximately 256,000 yen ($2,300). Details are as follows:

Given that the average monthly public pension received by an unemployed couple over 65 years old was 218,980 yen ($2,000) in 2020, the gap to be covered by personal savings would be approximately 36,000 yen ($330) per month or about 432,000 yen ($3,900) per year.

Assuming an average retirement of 25 years and no extraordinary medical expenses, on the surface it would appear that 10.8 million yen ($100K) would be required throughout retirement, which is only slightly more than the median amount saved by the time most people retire.

That would, however, be cutting it too close for comfort.

Most savings are kept in ultra-low interest savings accounts. Thus, capital appreciation is likely to be minimal. Unless Japan’s deflationary environment continues indefinitely into the future, which is highly unlikely, inflation is likely to eat into those savings to cause even more of a gap.

Potential Impact of Out-of-Pocket Medical Expenses

The big wild card is how to pay for medical expenses such as the cost of nursing care. According to the Ministry of Health, Labor and Welfare's "User Fees for Services," the monthly out-of-pocket expenses for a person who needs nursing care and moves into a welfare facility for the elderly (special nursing home) are 102,200 yen ($930) for a multi-bed room and 139,500 yen ($1,270) for a private unit-type room. The average length of stay in a long-term care welfare facility for the elderly tends to be about 4 years. The average cost for a multi-bed room is, therefore, approximately 1,220,000 yen ($11K) per year, or about 4,900,000 yen ($45K) over 4 years. For a private room the cost is about 1,670,000 yen ($15K) per year, or about 6,690,000 yen ($61K) over 4 years.

These fees are not covered by long-term care insurance. They are, moreover, per person. Thus, the overall cost would be double for a couple.

Bottom Line

Given all of these factors, the so-called “20 Million Yen Rule” is somewhat in the ballpark but still probably inadequate. The calculations include many assumptions which could vary wildly and, as a result, increase the amount of necessary expenses. Thus, a figure twice as high as the “20 Million Yen Rule” would probably be more appropriate—at a minimum.

Despite their reputation as faithful savers, at this point it would appear, therefore, as though most Japanese people do not have enough saved for retirement.

While work colleagues often obsess about each other’s compensation levels, perhaps Japan’s work compensation system itself needs to be examined. Levels of compensation now accepted as givens beg the question of what workers can do to change the system so their compensation levels can rise enough to be able to enjoy sufficient savings in retirement. The people’s culture is to be savers. But what is possible to save does not appear to be enough. How can that inequity be changed?

Links to Japanese Sources: 40代の7人に1人が「手取り16万円」…65歳から手にする年金は「月10万円」の衝撃 and 60歳で銀行口座に1,000万円…「貯蓄が尽きる」のはいつか?

its just crazy economics that these people spend so much on a depreciating asset, which they pay off over 30 years. money that couldve been invested in the stock market outside of japan.

I was thinking that the cost of living in Japan (generalizing) will need a lot more than the “20 Million Yen Rule” but it's interesting to compare with the 3% or 4% rule in the US.

The average 401(k) balance is $106,478, according to Vanguard's 2020 analysis of over 5 million plans and the median 401(k) balance is $25,775.