How Much Does an Emergency Room Visit Cost in Japan?

How Much Does an Emergency Room Visit Cost in Japan?

Examine a simple case to see how Japan’s system of national health insurance helps to keep out-of-pocket costs to a minimum.

Earlier this month on a Friday evening while quietly reading a book I was called from the kitchen by my wife. She calmly mentioned, “I may need you to take me to the hospital.” My immediate response was, “What? Are you okay? What happened?” Once again she calmly announced, “Well, I am okay, but I just cut the tip of my finger with a sharp knife, and I cannot seem to get the bleeding to stop. I may need stitches.” It did look pretty bad, as a fair amount of blood was gushing out of the wound.

As you can imagine, I immediately sprang into action, and we called the clinic where we had had our annual check-ups. While they said that they could see my wife, after hearing what had happened, the receptionist at the emergency room admitted that it might be best to go to another hospital with a surgeon because the physician on call that evening was an internal medicine doctor. That took us off guard for a moment. How would they handle a life-threatening emergency?

In any case, we pivoted quickly and called the nearest hospital that was a little bigger. They could, luckily, see my wife right away and had a surgeon available, if necessary. We were told to be certain to remember my wife’s insurance card, which, naturally, she always keeps in her wallet. We hopped in the car and sped off to this hospital that we had driven past many times but had previously never visited.

First, rest assured that my wife received high quality care right away and has subsequently made a full recovery. It turned out that the injury looked a lot worse than it was. She did not, in fact, need stitches!

Although the initial hiccup regarding where to go in case of an emergency was unanticipated, once we made it to the right hospital everything went smoothly. That little insurance card proved to be invaluable. It was her ticket to receive care quickly and efficiently. This is in large part thanks to Japan’s national health insurance plan, which is called kokumin kenko hoken (国民健康保険). It is available to all citizens and resident foreigners like me. Just to be clear, this is the type of government provided health insurance which is mandatory, unless one is already covered by kenko hoken (健康保険) or “employees’ health insurance” provided by most employers.

Although there have been significant modifications since the beginning of the program, Japan has had some form of national health insurance since 1922! Especially compared to the complicated system of private health insurance in the U.S., Japan’s national health insurance scheme seems to work reasonably well. This simple illustration will help you to understand our experience.

Cost of the Initial Consultation

On that Friday evening my wife was seen right away, patched-up, and sent along her way to the pharmacy next door to the hospital in short order. Before heading out the door she was, however, directed to pay-up in cash (some hospitals do, however, now take various forms of electronic payment).

She was provided with an out-patient receipt or gairai seikyu ryoshusho (外来請求領収書 see Exhibit A) and an itemized diagnosis/treatment bill or shinryo meisaisho (診療明細書 see Exhibit B). The bill was calculated by tallying up “points” to account for the cost of the provision of care as well as the cost of supplies. One point is equivalent to 10 JPY (US 9 cents). In my wife’s case the co-payment or “co-pay” was calculated at 30%, based upon our income. It can be as low as 20% for low-income patients.

Looking at the left column of Exhibit A it is possible to see that the overall number of points for the initial consultation totaled 413 (line highlighted in blue at the bottom). The total was composed of 293 points for the diagnosis and treatment (line highlighted in yellow), 68 points for disinfectant (line highlighted in green), and 52 points for the actual care provided (line highlighted in pink). The total was equivalent to 4,130 JPY ($37.50), and the co-pay was only 1,240 JPY ($11.25). Yes, you read that correctly. It was not $1,125 or even $112.50—only $11.25. The co-pay was calculated by taking 30% of the total (line highlighted in orange). That certainly seemed reasonable to us.

It would have been even lower had this not been the first time that my wife had ever visited this particular hospital.

Looking at Exhibit B it is possible to confirm that 288 points of the sub-total of 293 points were for the first-time use of the hospital or shoshinryo (初診料 line highlighted in yellow). 5 points were tacked on to cover the cost of infection control (line highlighted in green). I don’t know about you, but especially during a global pandemic adding 50 JPY (45 cents) for this valuable purpose seems acceptable. The remaining 68 points were for the disinfectant (line highlighted in blue), and 52 points for the actual wound care—including a bandage--which was calculated by the area of the wound (line highlighted in orange).

The physician on call wanted my wife to come back in a few days and in the meantime take oral anti-biotics. He also wrote a prescription for an optional pain killer. Thus, we were directed to walk over to the pharmacy next door to the hospital.

Pharmacy

It took only a few minutes for the pharmacy to fill the doctor’s prescription. The total fee came to 740 JPY ($6.67).

The format of the receipt from the pharmacy was almost identical to the documentation received from the hospital. All fees are calculated based upon the same point system. The “technical fee” for filling the prescription totaled 155 points (line highlighted in yellow), which was equivalent to 1,550 JPY ($14). Another 57 points (line highlighted in orange) were to cover “pharmacy management” expenses, and only 36 points (line highlighted in green) represent the actual cost of the anti-biotic. Thus, the total cost came in at 248 points (line highlighted in pink), which represented 2,480 JPY ($22.35).

The co-pay in our case was 30% or 740 JPY ($6.67).

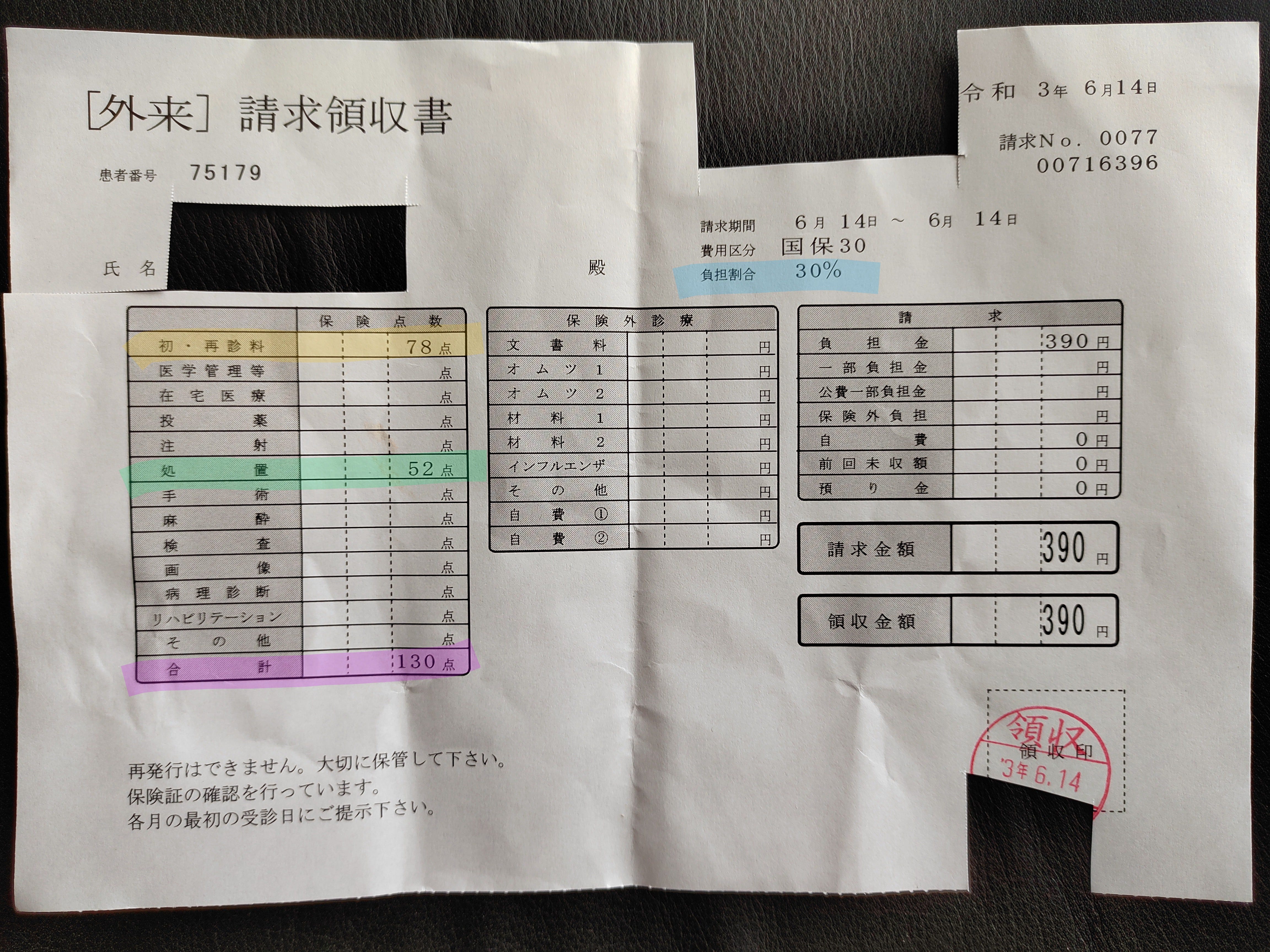

Follow-up Consultation

The doctor requested a single follow-up consultation a couple of days later to ensure that my wife’s finger was healing properly.

Just like before the receipt was easy to navigate and concealed no surprises. As listed in Exhibit D, 78 points were assessed for the diagnosis and treatment (line highlighted in yellow) and 52 points were charged for the actual care provided (line highlighted in green). Thus, the total cost of the follow-up visit came to 130 points (line highlighted in pink), which was equivalent to 1,300 JPY ($11.71). The 30% co-pay was, therefore, only 390 JPY ($3.50). As parking was free, the small co-pay covered all expenses for the visit.

Premiums

While these co-pay amounts probably seem fairly reasonable, you may wondering, “Yeah well, what about the premiums?” Given our semi-retired status, we must pay premiums directly to the local government office in charge of the national health insurance plan (as opposed to having an employer cover this cost by taking it out of a paycheck).

A general rule of thumb for calculating the annual premium is based upon taxable income (salary minus exemptions) – 330,000 JPY adjusted by health, support, and nursing care components. Rates vary slightly by municipality, and the actual premiums are billed in our town 7 times per year, which helps for managing cash flow.

While our specific premium is confidential, to get a better understanding of how much a typical premium costs, please refer to the following illustrations which were translated from the official government website for the program (http://www.kokuho-keisan.com/list/list.php?pref=44):

Model Case 1 (based upon rates for a city near our home)

Family Structure

Husband: Freelancer, age 43, annual salary of 5.5 million JPY ($49,500)

Wife: Homemaker, age 38

Son: Age 8

Daughter: Age 4

Other

Annual Tax for Fixed Assets (e.g., a home): 100,000 JPY ($900)

Premium (for the whole family of 4 people)

Annual: 600,000 JPY ($5,400)

Monthly: 50,000 JPY ($450)

While even these relatively reasonable rates could be a burden for some, even those who rely upon the gig economy tend to feel confident that they can support a family without having to worry unduly about the cost of medical care—especially if both spouses generate an income.

Premiums are much lower for elderly residents who have less income.

Model Case 2 (based upon rates for a city near our home)

Family Structure

Husband: Retired, age 73, annual pension of 2.2 million JPY ($20,000)

Wife: Retired, age 71, annual pension of 1.2 million JPY ($10,800)

Other

Annual Tax for Fixed Assets (e.g., a home): 80,000 JPY ($720)

Premium (for the whole family of 2 people)

Annual: 160,000 JPY ($1,400)

Monthly: 13,300 JPY ($120)

Given adequate planning and a reasonably frugal lifestyle, these rates should not break the bank.

The calculator behind these figures makes it easy to compare by geography. Rates for the same family structures tend to be, in general, fairly similar across the country, although rates in Tokyo and Saitama are, curiously, a relative bargain.

Key Take-away

Japan’s system of national health insurance not only helps to control costs in exchange for what tends to be, in general, excellent quality of care, but it provides peace of mind that medical bills will, most likely, not cause undo financial burden.

By this point you may be wondering what happened to my wife’s finger. I am happy to report that she has, luckily, made a full recovery, and is now just a little more careful when using a sharp blade in the kitchen.

Link to Japanese Source: http://www.kokuho-keisan.com/

Zato's been kicking around here for many years and a JP reader/speaker. but never have i seen as clear and concise an explanation of the JP national medical billing system as Mr. K. gives here. sincere thanks to Kennedy-sensei.

This article shows that healthcare is a right that is possible for a nation to provide for all of its citizens, without imposing undue hardship on them. And a healthier citizenship means a stronger nation.